Raport: Polish Warehouse Market 2022 summary and forecasts for 2023

AXI IMMO presents the report "Polish Warehouse Market - Summary 2022." 2022 in the Polish warehouse market was expensive, and 2023 may be even more expensive.

AXI IMMO presents the report “Polish Warehouse Market – Summary 2022.”

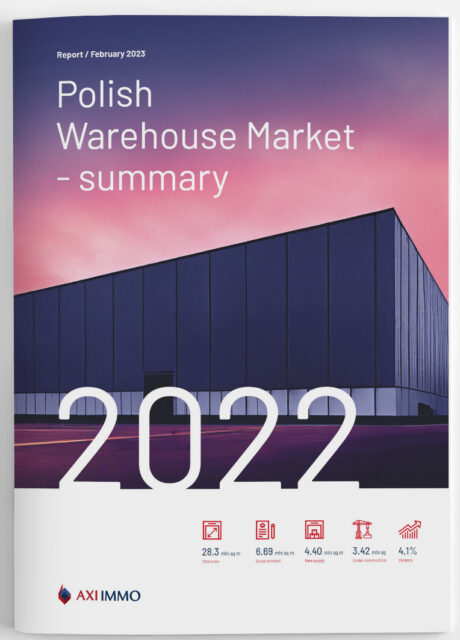

The Polish warehousing market in 2022 remained in good condition. By the end of December 2022, more than 4.4 million sqm (+42% y/y) of new space was completed, corresponding with strong activity by tenants, who leased nearly 6.7 million sqm (-9 y/y). Another 3.4 million sqm is under construction (-25% y/y), which promises to surpass the 30 million sqm mark in 2023. The high absorption rate did not significantly affect the increase in the vacancy rate, keeping it at 4.1% (+0.2 bps y/y). The event of the year was undoubtedly the rising rental rates, which increased on average by 15-20% compared to previous years.

The investment market in 2022 on the commercial real estate market

The volume of investment transactions in 2022 on the commercial real estate market closed at €5.8 billion. Of the total demand, the new leader was the office sector (36%), ahead of the warehouse (34%) and retail (26%). The total value of transactions involving industrial and logistics assets amounted to EUR 2 billion (-30% y/y). Traditionally, real estate portfolio acquisitions dominated the sales structure (42% of the volume). Among the largest transactions in the investment market in Q4 2022 was the sale of a BTS building by VidaXL (130,000 sqm) to Union Investment JV Garbe Industrial and Allianz’s purchase of the first tranche of properties owned by DHL (154,000 sqm). On the other hand, the number one acquisition of 2022 as a whole was portfolio acquisitions, including Hillwood’s Danica portfolio (629,000 sqm) acquired in Q3 2022 by CBRE GI, and a quarter earlier, Panattoni sold a portfolio of warehouse parks of about 500,000 sqm to EQT Exeter.

Grzegorz Chmielak, Head of Valuation and Capital Markets, AXI IMMO, says: “In 2022, despite the challenges of high inflation, the energy crisis or Russia’s renewed aggression in Ukraine in Poland, we recorded more than 120 transactions in the investment market. Significantly, five transactions accounted for 40% of the total volume. As usual, prime products in “core” and “core+” locations attracted the most interest. The high cost of financing caused investors to scrutinize the tenant mix in warehouse parks more closely than a year ago when making their purchase decisions. In 2023, we expect manufacturing properties to account for a larger share of the sales structure due to the growing importance of nearshoring and friendshoring trends.”

High demand in Tricity and Western Poland

At the end of 2022, the total volume of lease transactions in the Polish warehouse market amounted to 6.69 million sqm (-9% y/y). On the other hand, the so-called net demand, including only new contracts and expansions, contracted 4.48 million sqm (-20% y/y). In 2022, the largest warehouse space was leased in Warsaw at 1.38 million sqm, Upper Silesia at 1.22 million sqm, and Central Poland at 885,000 sqm. Noteworthy markets on the demand side remain Western Poland (440,000 sqm) and Tricity (325,000 sqm), which have seen increased transactions over the past three years. The former is due to its proximity to the German market, and the latter through its access to a seaport. Some of the largest deals in the October-December 2022 period include a new agreement signed by a confidential e-commerce tenant for 83,000 sqm at Mountpark Wrocław, the renegotiation of a logistics operator for over 60,000 sqm at P3 Piotrków, and a contract extension by Sistema at GLP Tychy Logistics Center Sistema (over 60,000 sqm).

E-commerce with the largest warehouses

In contrast, throughout 2022, the largest contracts signed were those with e-commerce customers. In Q2 2022, Best Secret decided to lease 90,000 sqm in a BTS building prepared by Panattoni, while two confidential tenants will occupy 83,000 sqm at the Mountpark Wroclaw logistics center (Q4 2022) and 82,000 sqm at Panattoni Park Poznań A2 (Q3 2022), respectively.

Anna Głowacz, Head of Industrial and Logistics, AXI IMMO, comments: “In 2022, we observed changes in the structure of demand. Invariably, logistics and retail chains will remain strong tenants, with a noticeable increase in interest in modern warehouse space by manufacturing clients. In 2023, we expect this trend to develop. Poland guarantees greatly understood business security and proximity to key sales markets. Among other active tenant groups, manufacturers and distributors of FMCG products and electronics, and to a slightly lesser extent e-commerce, should remain.”

E-commerce with the largest warehouses

Developer activity remained high in 2022, with a record 4.4 million sqm completed by the end of December (+42% y/y), which increased the total stock of warehouse space in Poland to 28.3 million sqm (+19% y/y). During the period under review, most new supplies were delivered in Lower Silesia at 787,000 sqm, Central Poland at 648,000 sqm, and Poznań and Upper Silesia at 540,000 sqm each. A selection of the largest logistics parks delivered between October and December 2022 included EQT Exeter Park Świebodzin – BTS OBI (108,000 sqm), which was also the largest completed project in 2022, as well as Hillwood Łowicz Południe (over 69,000 sqm) and Hillwood Zgierz (58,000 sqm). Under construction, in turn, is another 3.4 million sqm (-25% y/y), 46% of which are speculative projects. Completing the planned investments should allow Poland to exceed the 30 million sqm warehouse space mark in 2023.

Anna Głowacz explains: “In the second half of 2022, we observed a marked decline in warehouse projects started. The reduction in developers’ activity is mainly due to difficulties in obtaining financing. The current strategy of most investors is to launch projects only with a high share of pre-let contracts.”

The high performance on the demand and supply side did not significantly change the vacancy rate, which stood at 4.1% in Q4 2022 (+0.2 bps y/y). The provinces with the highest availability of warehouse space at the end of December 2022 were Lublin (9.5%), Lower Silesia (7%), and West Pomerania (6.4%). On the other hand, the hardest to find a vacant module was Pomeranian (0.8%) and Lesser Poland (1.2%).

What is the rental rate for a warehouse?

Phenomena such as high absorption rates, rising financing costs, and low vacancy levels have influenced the first significant increase in starting rental rates in the Polish warehouse market in years. The average increase in offered rates in 2022 in all regions fluctuated between 15-20%, with expectations of 30% more, mainly for new projects. Traditionally, Warsaw city remains the most expensive location in Poland, with average base rents of EUR 4.4 to EUR 7.0/sqm and effective rents in the range of EUR 3.8 to EUR 5.5/sqm. In other regional markets, average base rents ranged from EUR 3.5 to EUR 5.5/sqm and effective rents from EUR 2.7 to EUR 4.6/sqm.

Renata Osiecka, Managing Partner, AXI IMMO, concludes: “Despite the more difficult macroeconomic environment, 2022 surprised us positively with high demand results and a record in new supply. We are entering the next maturity phase, with the first signs of it brought by inflation, rising financing costs, and rising rents. The warehouse market has become tougher and more demanding. Tenants’ expectations are growing for new green leases that allow them to implement ESG strategies. In 2023, we will all be looking for optimization, solutions that guarantee real savings, where certification will no longer be a trend but a standard. The foundations of the warehouse sector will remain stable, with an expectation of reduced activity on the part of both tenants and developers. 2023 will be a time of review for the entire market.”

About AXI IMMO

AXI IMMO offers commercial real estate advisory services in leasing and managing industrial and office space, valuation, acquisition, and disposal of real estate assets and development land. The company also offers B2B and B2C supply chain management services. AXI IMMO’s most significant advantage is combining international service standards with thorough local market knowledge. The company received the award for the Best Local Agency in 2012-2019 and 2021 and the Best Team for the industrial sector in 2016-2017 in the prestigious CiJ Awards organized by the CEE CiJ Journal magazine.

Report — Polish Warehouse Market - Summary 2022

Download the report:

Recent articles

16 June 2026

AXI IMMO advises Logfret Poland – the logistics company moves to SEGRO Logistics Park Warsaw, Nadarzyn

4,900 sq m for an international logistics operator, with AXI IMMO advisory.

29 May 2026

AXI IMMO named Best Local Agency of the Year at CEEQA 2026

AXI IMMO has been awarded the Best Local Agency of the Year for the fourth time in a row

26 May 2026

Strong start to the year on the industrial market in Poland with a clear increase in new leases and expansions

AXI IMMO presents the report: “Industrial & Logistics Market in Poland, Q1 2026”

25 May 2026

AXI IMMO advises Tatuum on its relocation to Marq Logistics Łódź III logistics park

Polish fashion brand Tatuum has leased approximately 18,500 sqm in the eastern part of Łódź.